Australia’s Draft Digital Asset Laws: Implications for Financial Advisers, Insurers, and Big Super

Edited by Michael Prendiville and Hugh Fraser. Special thanks to Ben Ritchie from Alpha Node and Taylor McEvoy from Gallagher for their insights.

Four and a half million Australians held digital assets as of October 2025.[1] Most are Millennials and members of Gen Z. Among those who stay away, nearly half say the main reason is poor regulation. A global survey of institutional investors in 2025, mainly in the U.S. and Europe, found much the same: more than half said unclear regulation was the biggest barrier to investing in digital assets.[2]

Figure 1: Proportion of Australians holding digital assets (green) and those not holding them due to poor regulation (orange) as a share of the total population. Source: JellyC’s representation, based on Coinbase and EY-Parthenon survey data.

Australia follows the U.S. regulatory lead

Concern over weak regulation, long a source of uncertainty for investors and their advisers, is now being addressed globally. New U.S. regulations, including the GENUIS Act passed in June 2025, set strict rules for payment stablecoins, requiring them to be backed one-for-one by cash or high-quality liquid assets resembling those held by government money market funds. These developments are prompting other countries such as the EU’s MiCA, to reassess and upgrade their approach and regulatory regimes. The current U.S. administration also plans to classify digital assets as an alternative investment in 401(k) retirement plans, a move that could accelerate adoption, especially among younger workers who stand to benefit from compounding returns.[3]

In Australia the Federal Government released draft laws in September, primarily covering digital asset platforms and payment service providers. The first part introduces two new financial product categories: digital asset platforms (DAPs) and tokenized custody platforms (TCP). DAPs hold tokens on behalf of clients, for example, digital asset exchanges such as OKX and Independent Reserve. TCPs create tokens that represent rights to underlying assets and hold those assets in trust for clients. The second part covers payment service providers, such as stablecoin issuers or wallets that hold customer funds. Both draft laws would amend the Corporations Act 2001.

Figure 2: Market participants addressed in Australian Treasury Laws Amendment Bill 2025.

What the changes mean for financial advisers and super funds

These reforms are important for both financial advisers and their clients, as well as institutional investors and superannuation funds, with insurance playing a key role for both.

For years many advisers avoided digital assets because of their volatility. This now deserves a second look. For instance, when bitcoin and ethereum are compared with the one-year realised volatility of the “Magnificent Seven” tech stocks in the U.S., digital assets no longer appear uniquely or extremely risky. Similarly, volatility in other commodities and asset classes like gold, oil and gas has also been high.

Figure 3: Volatility comparison between Magnificent Seven, bitcoin, and ethereum.

Source: JellyC’s representation, based on Yahoo Finance data. Sample period: October 2024 to October 2025.

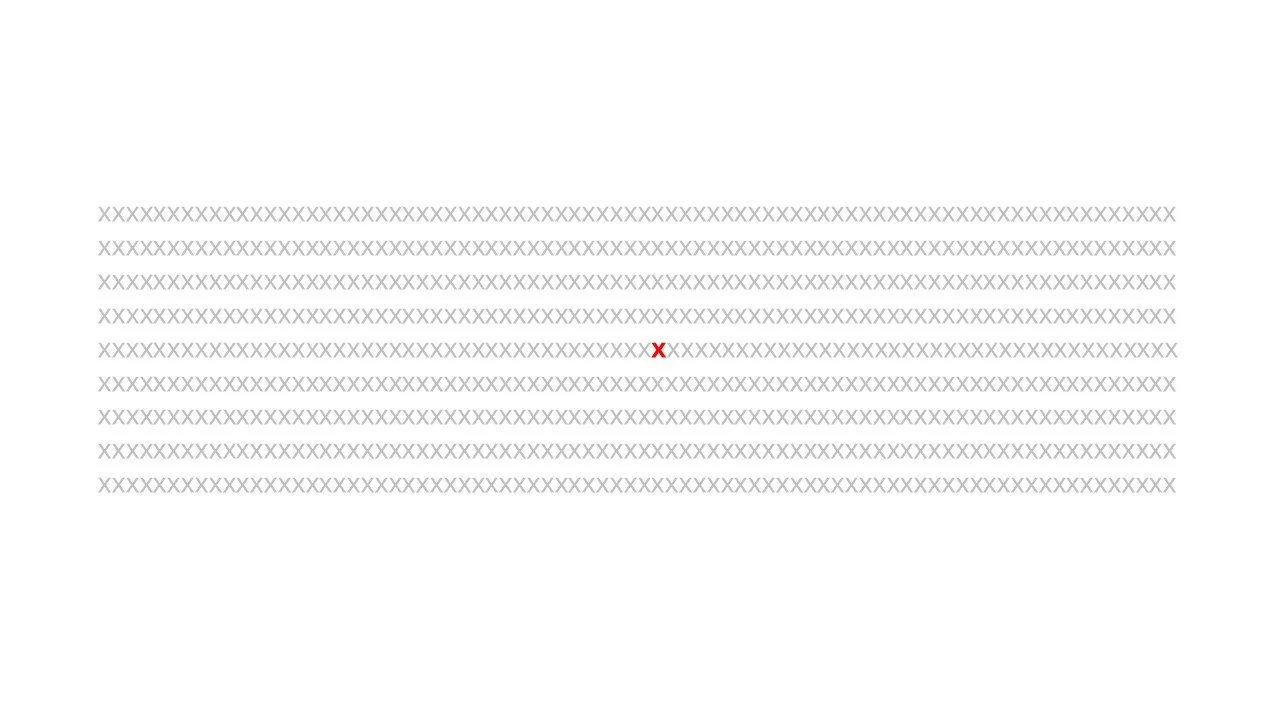

Another major area of concern around criminal use of digital assets appear overstated when looking at the latest data: in 2024, only 0.14% of on-chain transaction volume was tied to criminal activity, and ransom payments fell 35% from 2023 to 2024.[4] Stricter global KYC and AML rules, especially for custody platforms, have helped reduce illicit use. Given the widespread use of cash in criminal activity, fears about crypto now look overstated.

Figure 4: Out of 700 on-chain transactions visualised in grey, only one marked with a red ‘X’ was tied to criminal activity in 2024.

Source: JellyC’s representation, based on Chainalysis data.

Clearer and fit-for-purpose legislation and regulations, more effective policing of illegal transactions, and better risk management frameworks – for example, improved insurance coverage – will underpin the attractiveness of digital assets as an investment class and their place in investors’ portfolios.

This shift will create strong demand for digital asset education, research on appropriate portfolio allocations, and new insurance products. Because digital assets and blockchain work differently from traditional investments, advisers will need dedicated training to match clients’ risk profiles with the right level of exposure.

The education gap is the industry’s biggest structural barrier. It reflects challenges that advisers rarely face in traditional finance, such as digital custody arrangements, private key management, and technology risk. To address this, JellyC has developed an education program covering custody, private keys, risk, research, and portfolio construction. JellyC now delivers this education program to advisers and to investors new to the space.

The role of insurers

Insurance companies are the missing link connecting financial advisers with the wider adoption of digital assets by investment funds. Gallagher reports that financial advisers who work in the space are increasingly recommending digital asset exposure through exchange-traded products and managed funds. While most professional indemnity (PI) insurance policies still exclude digital assets, insurers are now more open to providing coverage when advisers have strong risk controls and limit exposure, usually 5-10% of the client’s portfolio.

JellyC estimates suggest that 10-15% of Australian financial advisers now have some form of digital asset insurance. Insurers’ due diligence processes typically assess the types of digital assets financial advisers work with, such as bitcoin or ethereum, the trading platforms used, and whether clients take custody of the assets themselves. Australia’s upcoming legislation will give insurers clearer rules to work with, helping them design products tailored to the specific risks of digital asset platforms and custody providers.

Figure 5: Triangular relationship between financial advisers, insurance companies, and super funds in providing coverage and access to digital assets.

What happens next?

Super funds are already moving. AMP became the first Australian super fund in 2024 to offer bitcoin exposure, using futures contracts to avoid managing digital asset wallets and specialist custodians. Its allocation amounts to 0.05% of assets under management, or roughly A$50 million. [5]

Momentum also builds in the U.S. In November 2025, Harvard University’s endowment fund, at nearly US$60bn assets under management the world’s largest, reported an almost 1% portfolio allocation to bitcoin for the period ending September 2025, aligning with BlackRock’s guidance that a 1-2% allocation is appropriate in diversified portfolios.[6]

Once Australia’s digital asset legislation is finalised, likely by mid-2026, advisers will have clearer rules, dedicated education pathways and fit-for-purpose insurance products. These pillars will extend Australia’s existing regulatory frameworks and accelerate the development of its digital asset ecosystem. Insurers will also gain the certainty they need to design tailored products, which will boost confidence among financial advisers and investment funds.

Regulatory clarity will remove one of the biggest barriers for both consumers and financial advisers. It will strengthen trust in the market, support Australia’s financial services and insurance sectors, and ultimately give Australians the option to access digital assets through their superannuation if they choose.

As blockchain-driven financial services transformation accelerates under initiatives such as Project Acacia, run by the RBA and the Digital Finance CRC, selective digital asset exposure offers both older and young Australians the opportunity to add a still-young asset class with a strong track record of value appreciation to their portfolios.

Younger Australians, already the most active adopters, stand to gain the most. Even small, professionally managed exposures can compound significantly over decades, offering a meaningful opportunity to build long-term wealth.

References

[1] Swyftx, 5th Annual Australian Crypto Survey, October 2025.

[2] Coinbase and EY-Parthenon, 2025, Increasing Allocations in a Maturing Market: 2025 Institutional Investors Digital Assets Survey, accessed 5 November 2025.

[3] The White House, Executive Orders, Democratizing access to alternative assets for 401(k) investors, 7 August 2025.

[4] Chainalysis, 2025 Crypto Crime Trends, 15 January 2025.

[5] AFR, This big super fund just became the first to buy into crypto, 12 December 2024.

[6] SEC, 13F-HR (Institutional investment manager holdings report), 14 November 2025.

Disclaimer

This article ("Article") has been prepared for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to purchase any financial product or service. This Article does not form part of any offer document issued by JellyC Pty Ltd (CAR Number 001293184), a corporate authorised representative of TAF Capital Pty Ltd (ACN 159 557 598, AFSL 425925). Past performance is not necessarily indicative of future results, and no person guarantees the performance of any financial product or service mentioned in this Article, nor the amount or timing of any return from it.

This material has been prepared for wholesale clients, as defined under Sections 761G and 761GA of the Corporations Act 2001 (Cth), and must not be construed as financial advice. Neither this Article nor any offer document issued by JellyC Pty Ltd or TAF Capital Pty Ltd takes into account your investment objectives, financial situation, or specific needs.

The information contained in this Article may not be reproduced, distributed, or disclosed, in whole or in part, without prior written consent from JellyC Pty Ltd. This Article has been prepared by JellyC Pty Ltd, which, along with its related parties, employees, and directors, makes no representation or warranty as to the accuracy or reliability of the information provided and accepts no liability for any reliance placed on it. Prospective investors should obtain and review the relevant offer documents before making any investment decision.